Introduction to Water Sustainability Reporting

Water has emerged as a central theme in sustainability reporting, with private sector water data disclosures seeing an 85% increase in the past five years (CDP, 2023). However, with business operations and suppliers spread across many regions, gathering the correct water data and meeting reporting requirements can take time and effort. This complexity increases for some reports requiring highly complex local, granular water data, such as business value at risk, risk response plans, and impact.

The good news is that this article can help you figure out where to start if you want to disclose your organization’s water risk and management practices.

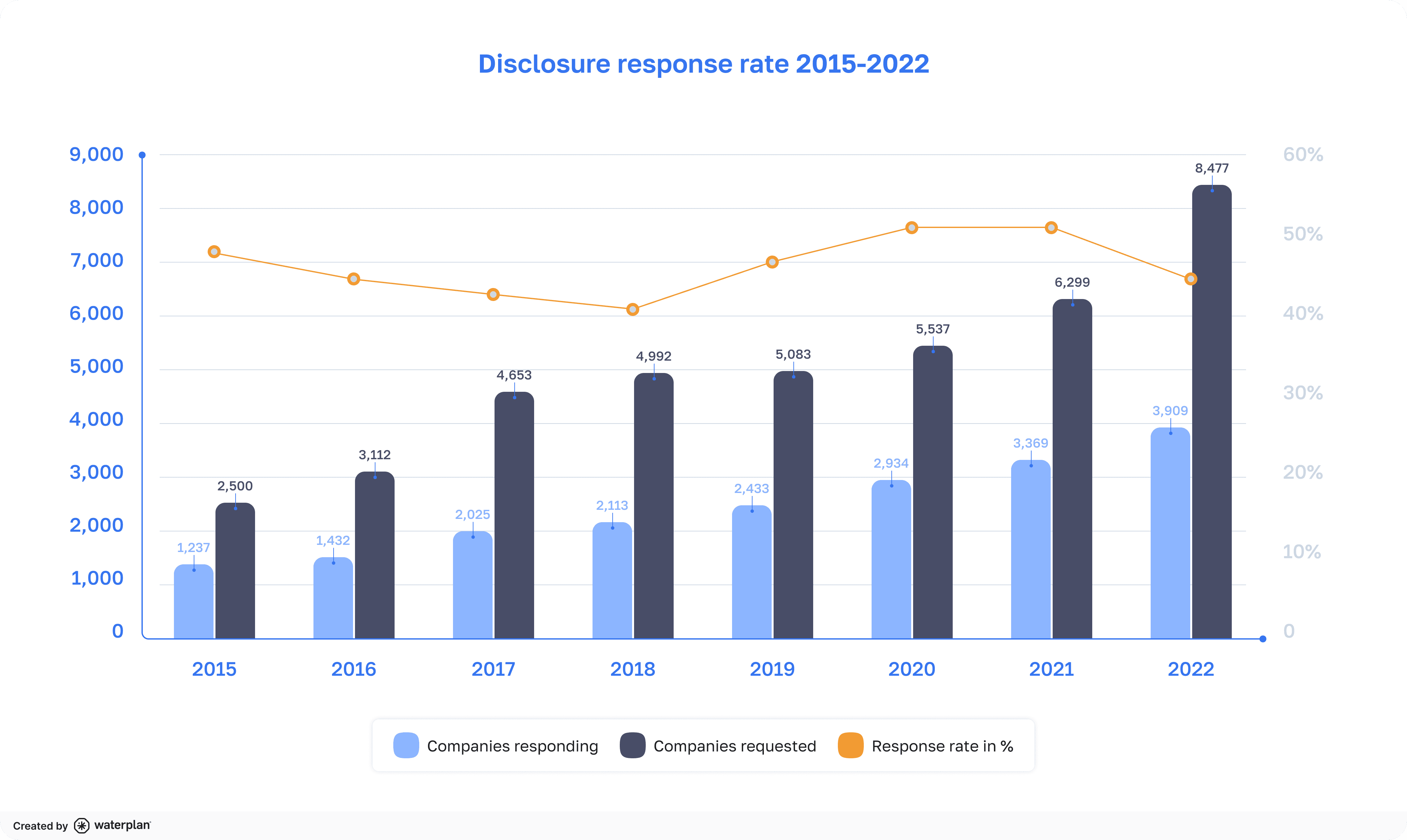

Evolution of companies disclosing water information to CDP.

Source: CDP Global Water Report 2022.

Why Report Water Data?

In many cases, companies disclose water data due to mandatory requirements, while in others, they do so voluntarily, driven by various factors.

Mandatory Disclosure:

Legal Requirement: Many jurisdictions mandate certain companies to disclose water management information such as the European Union, Canada, Japan, and New Zealand.

Stock Exchange Mandates: According to the UN Sustainability Stock Exchanges database, 37 stock exchanges globally require listed companies to report on environmental, social, and governance (ESG) factors, including water management practices.

Voluntary Disclosure:

Investor Demand: Given water's critical importance to many businesses, investors are increasingly interested in companies disclosing their water management practices. In 2022, 680 investors with 130 US$ trillion in assets requested companies to disclose water data (CDP, 2023).

Internal Performance: At some companies, senior management's performance review and non-salary bonuses are tied to the company meeting its sustainability goals, including water. According to a recent IBM survey, 50% of CEOs have their pay linked to Sustainability targets, a substantial increase from just 15% one year before.

Scoring: Some standard reports, such as CDP, assign scores or ratings based on various environmental indicators, including water usage and conservation efforts. These scores serve as benchmarks for evaluating corporate performance and influencing investor perceptions.

Improved Reputation: Corporations recognize the value of showing they are environmentally responsible entities. An improved reputation can help increase customer revenue and, at the same time, attract and retain talent, particularly in younger generations.

Types of Water Sustainability Reporting Requirements

There are multiple water sustainability reports, standards, and guidelines, each with varying requirements and timelines. The following are some examples.

Mandatory:

In Europe, the ESRS are mandatory standards for approximately 50,000 organizations based in Europe or foreign companies that have business in Europe. Regarding water disclosure, ESRS requires companies for which water is material, to disclose the sites with high water risk and the associated mitigation information.

In the US, the SEC’s Climate-Related Disclosure Rule has recently been adopted, requiring publicly traded companies with business in the US to disclose material climate-related risks, activities to mitigate or adapt to such risks, information on any climate-related targets or goals that are material to the business. The SEC estimates that 2,800 US and 540 foreign companies will have to report this information. Additionally, Form 10-K is mandatory for publicly traded companies in the US. This report requires companies to provide a comprehensive overview of their business and financial condition. Companies can voluntarily disclose information on water risk management in their 10-K report, but there is no specific requirement. Examples of companies that have mentioned sustainability information in their 10-K report are Mondelez and Cummins Inc.

Countries like New Zealand, the UK, and Japan mandate TCFD-aligned reporting for some companies. TCFD recommends companies that disclose information about climate-related risks and opportunities. Risks include changes in water availability, sourcing, and quality and increased severity of extreme weather events such as floods. Opportunities include increasing efficiency in water management and other risk mitigation measures.

Some countries are developing sustainability reporting standards, such as the UK (with the UK SDS) and Australia (with the ASRS). However, these are currently drafts under development, so the water data that will be required is still being determined. For instance, the UK SDS will be based on the ISSB standards, and it’s expected that it will be less extensive than the EU ESRS, which requires a “double materiality” assessment.

Voluntary:

Global reports and standards

The GRI 303 standard recommends organizations for which water is material to report information on water withdrawals, consumption, and discharges, as well as the organization's interactions with water as a shared resource. More than 10,000 organizations use GRI standards in over 100 countries.

The CDP Water Security questionnaire requires companies to disclose water withdrawals, consumption, discharges, water-related risks, water targets, and performance metrics. CDP assigns scores based on environmental performance, and one of the scores is related to water security. In 2022, 3,909 companies disclosed water-related data through CDP, and only 101 of them got the best water security score.

ISSB Standards (by the IFRS) aim to establish a global baseline for sustainability reporting and start being applied in 2024. ISSB builds on TCFD recommendations, the Integrated Reporting Framework, the CDSB Framework, SASB Standards, and the World Economic Forum’s Stakeholder Capitalism Metrics. There are two ISSB Standards that require water information. IFRS S1 recommends disclosing sustainability-related risks and opportunities over the short, medium, and long term. IFRS S2 provides more detailed disclosures to be used with IFRS S1. This standard specifically focuses on climate mitigation and climate adaptation.

SASB has developed more than 70 industry-specific standards for financial reporting that 3,100 companies use in more than 80 jurisdictions. The combination of SASB and ISSB can offer a comprehensive and detailed approach to sustainability reporting, particularly from an industry-specific perspective. While the ISSB provides overarching sustainability standards globally, SASB's industry-specific metrics allow for a deeper dive into sector-specific issues and performance indicators.

TNFD has developed a set of disclosure recommendations to assess, report, and act on nature-related dependencies, impacts, risks, and opportunities, which include water management, risks and opportunities. 319 organizations intend to start making disclosures aligned with the TNFD Recommendations by the financial year 2024 (or earlier) or 2025.

The Science Based Targets for Freshwater (part of the SBTN) guide companies in assessing freshwater management and associated water risks, prioritizing water-related challenges, establishing targets to address them, and tracking their impact. Additionally, there are Science Based Targets for Nature that require some information on freshwater.

The 17 Sustainable Development Goals (SDG) developed by the UN and adopted by multiple countries and companies emphasize sustainable development's interconnected environmental, social and economic aspects. Multiple SDGs are directly linked to corporate water management, including SDG 6 (Clean Water and Sanitation), SDG 13 (Climate Action), and SDG 14 (Life Below Water). Based on a survey by KPMG, in 2022, 71% and 74% of the N100 and G250 companies reported adoption of the SDGs. Additionally, the World Benchmarking Alliance develops benchmarks that compare companies’ SDG performance.

ISO 26000 guides “the right thing to do” for society and the environment. This international standard recommends sustainable water management across operations and supply chains, including water consumption, withdrawals, and quality. Unlike other standards of this organization, ISO 26000 cannot be certified. More than 85 countries have adopted this standard as a National Standard.

Certifications

ISO 14001 is an internationally recognized standard that provides a framework related to environmental management, which includes water. Particularly, ISO 14002-2 offers guidance for implementing ISO 14001, focusing on managing environmental aspects and conditions related to water. This encompasses conducting a water review to identify dependencies, risks, impacts, and issues about water, establishing objectives, measuring and monitoring parameters affecting water-related risks, devising emergency plans, and responding to adverse water-related environmental conditions.

The Alliance for Water Stewardship (AWS) requires companies to demonstrate adherence to the AWS Standard 2.0, which entails understanding water dependencies and impacts and the development, implementation, and measurement of risk mitigation strategies. The Standard is site-based and applicable globally to all organizations and industrial sectors, independent of their size and operational complexity.

International indexes and rating systems.

Examples that assess companies' sustainability performance for investors are DJSI, MSCI ESG Ratings, EcoVadis, S&P 500 Environmental & Socially Responsible Index, FTSE4Good Index, and STOXX. Companies with superior water management practices typically receive higher ratings. The type of water data that these systems evaluate varies. For example, MSCI ESG Ratings assess companies based on the water intensity of their operations, the water stress in their operations, and their efforts to manage water-related risks.

Roundtables and Membership Groups

Some organizations recommend that their members report sustainability information, including water management. Examples are BIER, which focuses on sustainability issues specific to the beverage industry; ICMM, which issues guidelines for responsible mining practices; IPIECA, which provides sustainability reporting guidance for the oil and gas industry; CGF, which developed guidelines for the CPG industry for disclosing product sustainability information; and the Water Resilience Coalition.

Corporate reporting

Finally, most organizations also develop reports in which water data is included, such as the Sustainability Report, the Water Policy, regular reports, and one-pagers for leadership. In this case, the type of data to report depends on each company. Based on a survey by KPMG, in 2022, 96% and 79% of the N100 and G250 companies reported on sustainability.

Where Should You Start?

With so many reporting frameworks and standards in place, determining where to start can seem daunting. The first step is to identify the mandatory requirements for your business to ensure compliance. Afterward, you can assess whether any voluntary reports align with the goals and needs of your organization and consider disclosing information for these reports, too. Additionally, seeking guidance from experts in the field or engaging with industry networks can provide valuable insights and support in selecting the most suitable reporting approach.

The Water Reporting Journey

Different teams can disclose water information depending on the company and the type of report, such as Investor Relations, ESG, EHS, Sustainability, and Environmental teams.

The process doesn’t significantly vary from one report to another. However, the time required, the granularity of data needed, and the number of stakeholders involved can differ. When considering disclosure of water-related information across different reports, it's crucial to identify those with overlapping requirements to enhance efficiency in planning efforts.

Generally, the water reporting journey involves the following steps:

Reviewing reporting requirements and conducting a gap analysis

Each year, corporate teams review their reporting requirements and conduct a thorough gap analysis to pinpoint any newly required data that wasn't necessary in the previous year. This process involves crafting a detailed plan for gathering this additional data, leveraging both internal resources and external data sources. This step is critical to ensure compliance with current standards and regulations.

Gathering data with the right level of granularity and frequency

This is generally the most time-consuming and complex step, where water data availability and centralization, as well as water expertise, are critical factors in reducing the time spent. Depending on the processes and systems in place, some companies may require multiple tools and stakeholder interactions across teams to gather and centralize the appropriate data.

Data to be gathered can include water withdrawals, consumption, and water quality in the most basic reports, water-related risks, value at risk, risk response plans, and water targets and stewardship activity impact data on the most thorough water security reports.

Data consolidation

Once water data across operations is collected, it must be consolidated into a single picture at a facility, region, and company level. As the types of water data to be disclosed are similar across reports, there is no need to repeat this step for all reports in many cases.

Completing the report

Reports often require similar data but in different formats, so the information completed for one report can be repurposed for another. For example, the water data required by CDP Water Security is more comprehensive than the data needed by GRI 303, so synergies can be leveraged if a company reports to both.

Review and approval

After completing the report, the information is reviewed to ensure the data and language are accurate, especially for external reports. Many stakeholders participate in this step, typically involving legal, communications, and leadership.

Publication / Submission

Once the report is finalized, it is submitted or published in the appropriate communication channel. For example, CDP Water Security is submitted through the integrated CDP Questionnaire, and Sustainability Reports are typically published on each company’s website.

Stakeholders in Water Reporting

Multiple internal and external stakeholders play a crucial role in the process. For example:

Internal Stakeholders:

Several corporate, regional, and facility teams are involved.

Board of Investors: Often, sustainability reporting is driven by investors’ demand.

C-Suite: They can also drive sustainability reporting. Additionally, they will receive most internal water sustainability reports and will be vital in approving external reports before their submission or publication.

Investor Relations: Responsible for maintaining communication with investors regarding sustainability initiatives.

Corporate Sustainability Teams: This team leads the overall sustainability strategy, initiatives, and reporting efforts. This team can collaborate with EHS, investor relations, and others for some reports.

Corporate Water Lead: Present in some organizations, this stakeholder drives water sustainability strategy, initiatives, and reporting.

Regional Environment, Health, & Safety (EHS) and/or Sustainability Teams: These teams usually help gather and consolidate water data from different facilities, following the plan outlined by the corporate team.

Facility EHS and/or Sustainability Managers: They gather the required water data from the facility and share it with the regional or corporate teams.

Legal and External Communications Teams: They review the preliminary reports to ensure compliance, credibility, and overall alignment with organizational messaging.

External Stakeholders:

Regulatory Bodies: Mandate companies to disclose water-related information and, in many instances, take action concerning water risks—for example, the European Parliament in the European Union.

Non-Governmental Organizations (NGOs): Typically raise awareness on water-related issues and may influence regulatory changes. An example is Water.org, which has participated in the Water Resilience Coalition, raising awareness about the importance of universal access to sanitation and water.

Value chain: Advanced water stewardship companies may request their suppliers or customers to disclose water data. According to CDP's 2022 Global Water Report, 33.8% of companies disclosing water information requested 50% or more of their suppliers to report their water use, risks, and management information.

Consumers: Demonstrate growing interest in companies' sustainability efforts, especially in younger generations. A recent study by Harvard mentions that when Gen Z and Millennial customers believe a brand cares about its impact on people and the planet, they are 27% more likely to purchase it than older generations.

Frequent Challenges & Opportunities

Main Challenges

Continuously Evolving Regulatory and Reporting Landscape

As water becomes increasingly integrated into overall sustainability reporting, it is subject to various evolving frameworks and standards.

Sustainability managers face the challenge of staying well-informed amidst this dynamic environment. They must cultivate networks and continuously update their knowledge to adapt to changing requirements. Failure to adhere to updated reporting requirements could result in reputational damage, lower scores, or investor scrutiny.

Looking ahead to 2024 and 2025, several emerging standards and regulations are on the horizon, including industry-specific standards within the ESRS and GRI, and the UK SDS. As these reports are still in development, the specific requirements for water data still need to be clarified. However, companies should stay informed and report the necessary information once these standards are finalized.

2. It's Time-Consuming, Specifically Gathering Water Data for Reporting

The time spent preparing standard reports, such as CDP Water Security, is significant, ranging from several weeks to months, depending on factors like data availability and the processes to gather and report water data. This extended duration is primarily due to the specificity and complexity of gathering granular water data at the facility level.

Organizations typically rely on manual procedures to gather, assess, and structure the data, which, combined with approval processes, contribute significantly to the time spent on reporting. Occasionally, companies engage external consultants to assist in local data collection and report development. However, their services can be expensive, potentially hindering access for some organizations.

The Opportunity of Leveraging Technology

Technology offers promising solutions to address these challenges, revolutionizing water sustainability reporting.

Keep organizations informed about the latest reporting requirements in different industries or regions.

Gather local water data at the right granularity, frequency, and accuracy level.

Automate water data-gathering processes at various levels, from corporate facilities to regional and global scales.

Structure water data according to the format required by different types of reports.

Improve efficiency in review and approval processes by enabling real-time collaboration among stakeholders.

Carbon & Water Disclosure

Although carbon and water sustainable management are key pillars to address climate change, carbon reporting is more prevalent than water reporting in corporate sustainability practices. Consequently, there is a broader array of resources guiding carbon disclosures and greater availability and adoption of technology solutions that streamline the carbon reporting process.

This is primarily due to:

Difference in Awareness: The awareness surrounding carbon's impact on climate change is much higher, as evidenced by regulations mandating action and disclosure from companies. In contrast, awareness about how climate change affects water resources is lower, resulting in fewer regulations requiring water disclosure. This also leads to a disparity in technology adoption, with more solutions available for tracking and reporting carbon data compared to water.

Water is local: Water problems vary depending on the region. Companies require local data assessment, which is typically complex and requires specific expertise to assess and disclose water data. As a result, many companies need help to determine their water risks accurately.

Conclusion

The significance of water reporting extends beyond mere information disclosure. Raising awareness about water-related challenges is essential to helping organizations and governments prioritize and address these issues transparently and collaboratively. Water reporting is a powerful tool that can drive collective action and ultimately contribute to positive change, ensuring access to water for all. Corporate sustainability teams play a crucial role in this process, utilizing water reporting to guide strategic decision-making within their organizations, foster stakeholder engagement, and drive positive change toward a more sustainable and resilient future.

ブログ

Get insights, expert analysis and tips on measuring, reporting, and responding to water risk